{kind=link}

In this post, I’ll talk about The Crypto Super-App and how sites like Coinbase and Revolut are developing into comprehensive financial ecosystems rather than just wallets.

These apps seek to become the “WeChat of the West,” transforming digital finance through integration, ease, and innovation in a world economy that is changing quickly. They cover everything from cryptocurrency trading and payments to banking and Web3 access.

What Is a Super-App?

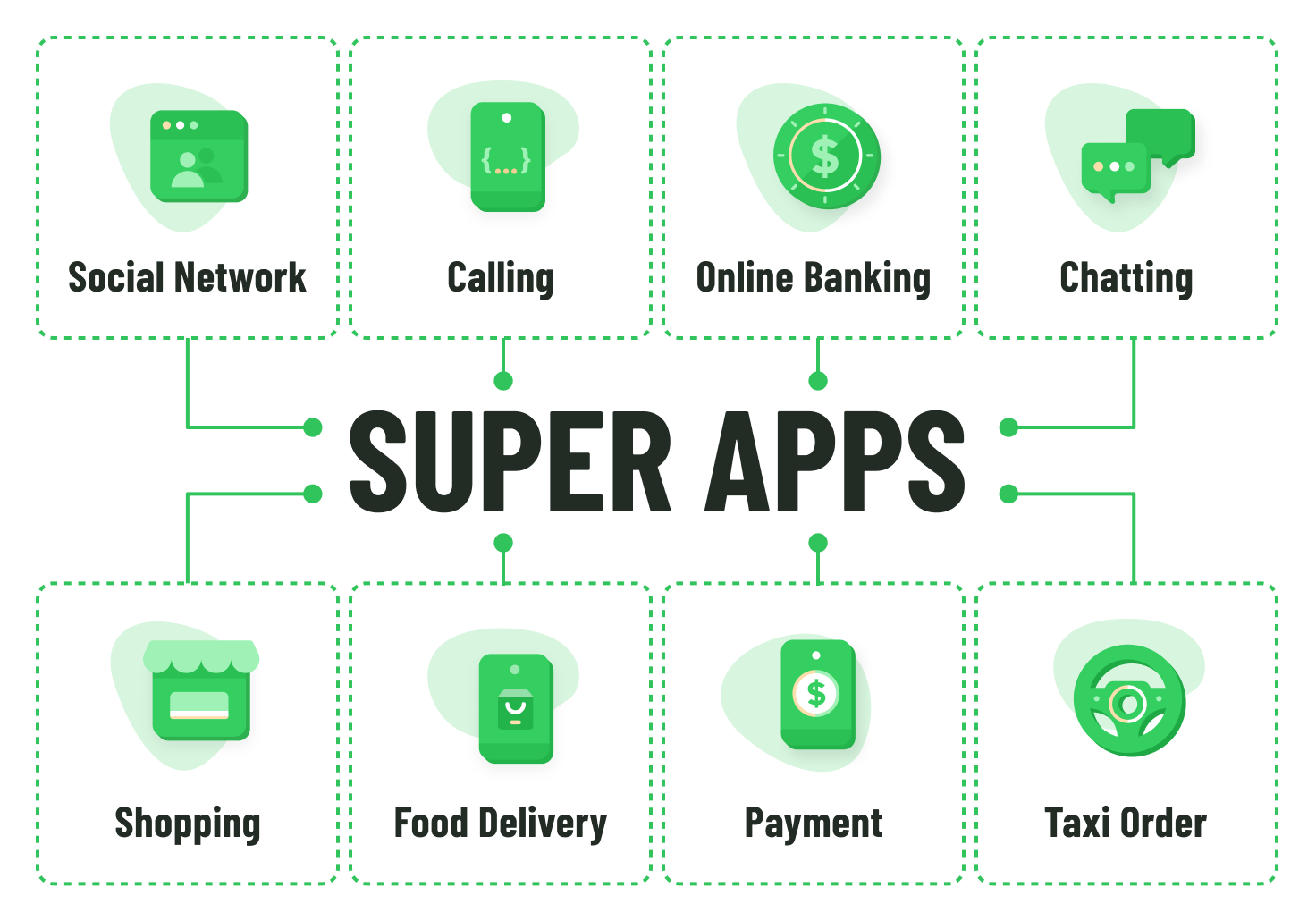

Super-apps enable users to do most of their daily digital activities without switching between multiple platforms. As an integrated digital tool, super-apps offer digital payments, messaging, online shopping, transport services, banking, online entertainment, and other services via external partnerships and mini-apps.

The opposite of a super-app is a traditional app, with one primary purpose. For example, a banking app that allows you to transfer money or a ride-hailing app to order a taxi. While some traditional apps can become a super-app by acquiring other services, super-apps are usually purpose-built from the ground up.

The strongest network effects are realized when there is the most number of users and enterprises, so the most users join the super-app to use a service. The most frequently mentioned example of a super-app is China’s WeChat. WeChat includes messaging, payments, loans, investments, ride-hailing, and e-commerce services, and even government services, all through the same app.

Super-apps, for their primary goal of providing the greatest user ease, have embedded finance, integrated data across service, and so ecosystem lock-in. As a result, users are able to move between services, and companies gain from a greater level of consumer engagement and data for monetization.

Evolution of Crypto Wallets

Private Key Wallets

The first version of crypto wallets were created just so customers could store private keys in order to send and receive Bitcoin. Simple wallets also provided little information to users because interfaces had no additional functions like being able to send and receive other currencies.

Portfolio Management

As wallets developed, new functions were added to allow customers to manage multiple portfolios in just one wallet. This eliminated the need to create new wallets for other chains and to manage the portfolios.

User Interface Improvements

The introduction of mobile applications, biometric security, seed phrase backups, and simplified interfaces also advanced wallets. This made the use of crypto wallets available to people outside technical circles.

Wallet and Exchange Application

The integration of exchange applications with wallets created a new functionality of allowing users to purchase, sell, and exchange crypto without having to leave their wallets.

Crypto Wallet and DeFi Integration

Along with advanced functionalities, wallets also integrated with the Web3 to support DeFi, NFTs, and dApps, along with added functions for staking, yield farming, and other crypto services.

Crypto Wallets and Traditional Finance

The collaboration between wallets and banking services has enabled the exchange of traditional money with crypto, and combined the services of traditional banking with crypto.

Crypto Wallets and Security

Development in hardware wallets, multi-signature functionality, and other encryption technologies created more secure wallets to combat the growing security issues of crypto.

Super-App Features

The current top wallets are integrating debit cards, cross-border payments, portfolio analytics, stablecoins, trading stocks or commodities, etc. Also, trading stocks or commodities offers stock trading functionalities to position themselves as super financial apps.

AI and Personalization

New AI tools in wallets to provide portfolio insights, fraud detection, categorize transactions, automate certain strategies, etc. in addition to growing intelligent financial assistants.

Comparison: WeChat vs Western Crypto Apps

| Feature / Aspect | WeChat (China) | Coinbase (US) | Revolut (UK/EU) |

|---|---|---|---|

| Core Identity | Messaging-based super-app | Crypto exchange + wallet | Digital banking super-app |

| Messaging | Full-featured chat, voice, video | No native messaging | Limited (basic in-app chat/support) |

| Payments | WeChat Pay (QR, P2P, merchants) | Crypto payments, stablecoins, card | Fiat & crypto payments, global transfers |

| Banking Services | Loans, wealth management, insurance | Limited (crypto-focused services) | Full banking features (accounts, IBAN, cards) |

| Crypto Services | Limited (restricted in China) | Trading, staking, custody, Web3 | Crypto trading, limited staking |

| Mini-App Ecosystem | Extensive third-party mini programs | Limited Web3/dApp integration | Limited partner integrations |

| E-commerce | Deep integration with merchants | Indirect (crypto commerce tools) | Integrated shopping perks & cashback |

| Cross-Asset Trading | Primarily financial products in-app | Crypto-focused | Stocks, ETFs, commodities, crypto |

| Government Services | Yes (public services integration) | No | No |

| Geographic Reach | Primarily China | Global (strong in US/EU) | Global (strong in Europe) |

| Regulatory Environment | Centralized under Chinese regulation | Heavily regulated in US | Regulated under UK/EU fintech laws |

| Network Effects | Extremely high (daily-life dependency) | Strong within crypto ecosystem | Strong within fintech ecosystem |

| Super-App Maturity | Fully established | Emerging | Semi-established |

Key Features Driving Super-App Status

All-in-One Ecosystem

A Super-App integrates several services like payments, trading, banking, shopping, etc., into one platform so users don’t have to switch between apps.

Seamless User Experience (UX)

Smooth service transition facilitates intuitive and engaging interface. This increases time spent daily on the App by users.

Integrated Payments Infrastructure

Payments (fiat, crypto, and stablecoins) and P2P, merchants, subscriptions, and cross-border transactions can be processed within the App.

Cross-Asset Financial Services

Providing services on diverse assets, be it crypto, stocks, commodities, savings, and loans, makes the App a one-stop shop for financial services.

Embedded Finance Capabilities

Services like loans, insurance, staking, and yield products are incorporated a** d within the platform, not offered as third-party services.**

Third-Party Mini-App or Partner Ecosystem

External services or mini-apps can be incorporated to build a more functional, digital, and integrated ecosystem around the core platform.

Strong Network Effects

More users, merchants, and developers on the App increases value, resulting in exponential growth, retention, and triggering more customers to join.

Data-Driven Personalization

Financial decision making is enhanced as users are engaged more. This is the result of personalized offers, portfolio insights and analysis, and targeted recommendations powered by AI.

Security and Trust Infrastructure

Trust built with advanced encryption and compliance frameworks, integrated fraud detection, and regulatory compliance is essential for scalable financial services handling.

Scalability and Global Reach

The ability to operate across legal boundaries, support multiple currencies, and manage large transaction volumes is essential for super-app dominance.

Opportunities

Mass Adoption of Cryptocurrency

Super apps can ease the cryptocurrency onboarding process by incorporating KYC and wallet solutions and methods for seamless electronic/fiat-currency conversion. By simplifying the process, super apps can induce cryptocurrency adoption by more than just users who are tech-savvy.

Empowering Users with Banking Needs

Super-apps can empower users with banking needs by enabling access to banking, payment, saving, lending, and cryptocurrency within a single application.

Disruption of Cross-Border Payments

Global remittance flows present enormous market opportunities due to the use of stablecoins and the blockchain for cross-border payment transactions as opposed to traditional banking systems.

Tokenized Real-World Assets (RWAs)

Super apps will create a 24/7 global marketplace by providing access to tokenized stocks, bonds, and real estate.

Integration of the Creator and Gig Economy

The wallet of a super app enables instant payouts, microtransactions, NFTs, and digital ownership to the creators and freelancers.

Embedded DeFi Services

DeFi services like lending, staking, yielding, and decentralized exchanges may be provided within a regulated environment.

Management of Finances with Artificial Intelligence

Super apps will have AI assistants that offer portfolio optimization, risk alerts, budgeting, and automated investment strategies.

Merchant Ecosystem Expansion

In-app payments, loyalty programs, and acceptance of cryptocurrency by merchants can create a closed-loop commerce ecosystem.

Digital Identity and Web 3.0 Integration

Wallet-based identity systems can be used for authentication, reputation systems, and decentralized logins.

Convergence of Fintech and Web3

The fusion of conventional banking systems and blockchain technology has the potential to transform super-apps into cutting-edge global financial systems.

Challenges and Limitations

Regulatory Uncertainty

There are multiple regulations concerning compliance across different jurisdictions for crypto and financial technology, which further makes it challenging to provide services globally.

Licensing and Legal Barriers

Integrating banking, trading, payments, and crypto services into a single platform means paying for several licenses, which increases operational expenses and legal liabilities.

Security Risks

Having several financial services in one application means more and more users are more likely to be targeted by hackers, phishing, and fraud.

Trust and Custody Concerns

Users generally do not want to store a significant amount of digital and traditional cash in one single centralized ecosystem.

Fragmented Western Markets

Western markets are divided competing platforms unlike China where the digital ecosystem is unified. This means less influence through network effect.

Competition from Big Tech and Banks

Financial service offerings from firms such as Apple, Google, PayPal, and other financial institutions are providing more competition.

Interoperability Challenges

Effective and smooth user experiences remain complex in a variety of ways.

User Privacy Issues

Supertaps have long track records of collecting and utilizing integrated and behavioral data, the concern is unmonitored dataexplosions and law compliance.

Future Outlook

Clearer regulations, the use of stablecoins, and a closer connection between blockchain technology and conventional banking will probably influence the development of crypto super-apps in the West in the future.

Platforms like Coinbase and Revolut may develop into full-fledged digital financial ecosystems as opposed to stand-alone trading apps when tokenized real-world assets, AI-driven financial assistants, and embedded DeFi services advance.

However, Western markets are still fragmented and heavily regulated, which makes the emergence of a single dominant super-app less certain than China’s unified market, which allowed WeChat to dominate. Rather, a few strong regional firms might integrate digital identification, payments, banking, and cryptocurrency into smooth platforms that eventually supplant conventional financial apps.

Conclusion

The emergence of the Crypto Super-App signifies a dramatic change in the way that digital finance is provided and utilized. Platforms such as Coinbase and Revolut are developing into complete ecosystems that include Web3 access, trading, payments, and banking in a single interface, going beyond simple exchanges or fintech apps.

The tendency is clear: finance is merging into unified, app-based ecosystems, despite the legislative, cultural, and competitive obstacles to replicating WeChat’s supremacy in the West.

The Crypto Super-App has the potential to revolutionize global financial infrastructure and serve as the entry point to the upcoming digital economies if these platforms are able to effectively strike a balance between innovation, compliance, security, and user trust.

FAQ

What is a Crypto Super-App?

A Crypto Super-App is a digital platform that combines crypto wallets, trading, payments, banking, and Web3 services into one unified ecosystem, allowing users to manage multiple financial activities within a single app.

Why is it compared to WeChat?

WeChat integrates messaging, payments, shopping, and financial services in one app. Similarly, crypto super-apps aim to centralize finance, trading, and digital services into a seamless platform experience.

Are Coinbase and Revolut considered crypto super-apps?

They are emerging versions. Coinbase focuses on crypto trading, staking, and Web3 access, while Revolut blends banking, payments, stocks, and crypto into a multi-asset fintech platform.

How do crypto super-apps generate revenue?

They earn through trading fees, payment processing, subscription plans, staking commissions, lending spreads, interchange fees from cards, and partner integrations.